In the time I've spent as a financial advisor working to help our members secure their personal finances, “When is a good time to start investing?” is one of my all-time favorite questions.

As with most personal finance topics, the answer depends on your financial situation. But for many people, the short answer is now. Time is on your side.

Read on for four reasons why it may make sense for you to start investing sooner rather than later.

Reason 1: There's a time value of money.

Reason 2: Get the most out of your money with compounding.

Reason 3: Your financial house is in order.

Reason 4: You have access to retirement accounts.

Reason 1: There's a time value of money.

We hear this phrase tossed around a lot. It means that money in the present is worth more than money in the future. Why? Because inflation causes money to lose its purchasing power.

To illustrate the time value of money, let's take a little field trip back to 1952. To set the scene, the first Chevy Corvette prototype was just completed and the first Mr. Potato Head flew off the shelf.

That year, if I were to buy one gallon of milk and five gallons of gas, it would have cost $1.96. Compare that to today, where the same purchases would run me about $18.97.

Why is time value of money important?

As we see from this example, prices tend to increase over time. One dollar 30 years from now won't buy as much as one dollar today.

We all instinctively understand that. That's why we invest. Our goal is to earn a return that outpaces inflation, so that our money doesn't lose its purchasing power over time.

There's another reason why a dollar today is worth more than a dollar in the future: It has earning potential. With successful investing, we all hope to turn $1 into $2, and then $3, $4, etc. If I have $10,000 today, my goal is to use that to earn a return that outpaces inflation, so that my money is worth more than $10,000 20 years from now.

How do we accomplish that? Through the power of compounding.

Reason 2: Get the most out of your money with compounding.

When we invest our money, we hope that our money will earn more money, and that money will earn money, and so on and so forth. Our gains come not only from our initial principal, but also from our earnings.

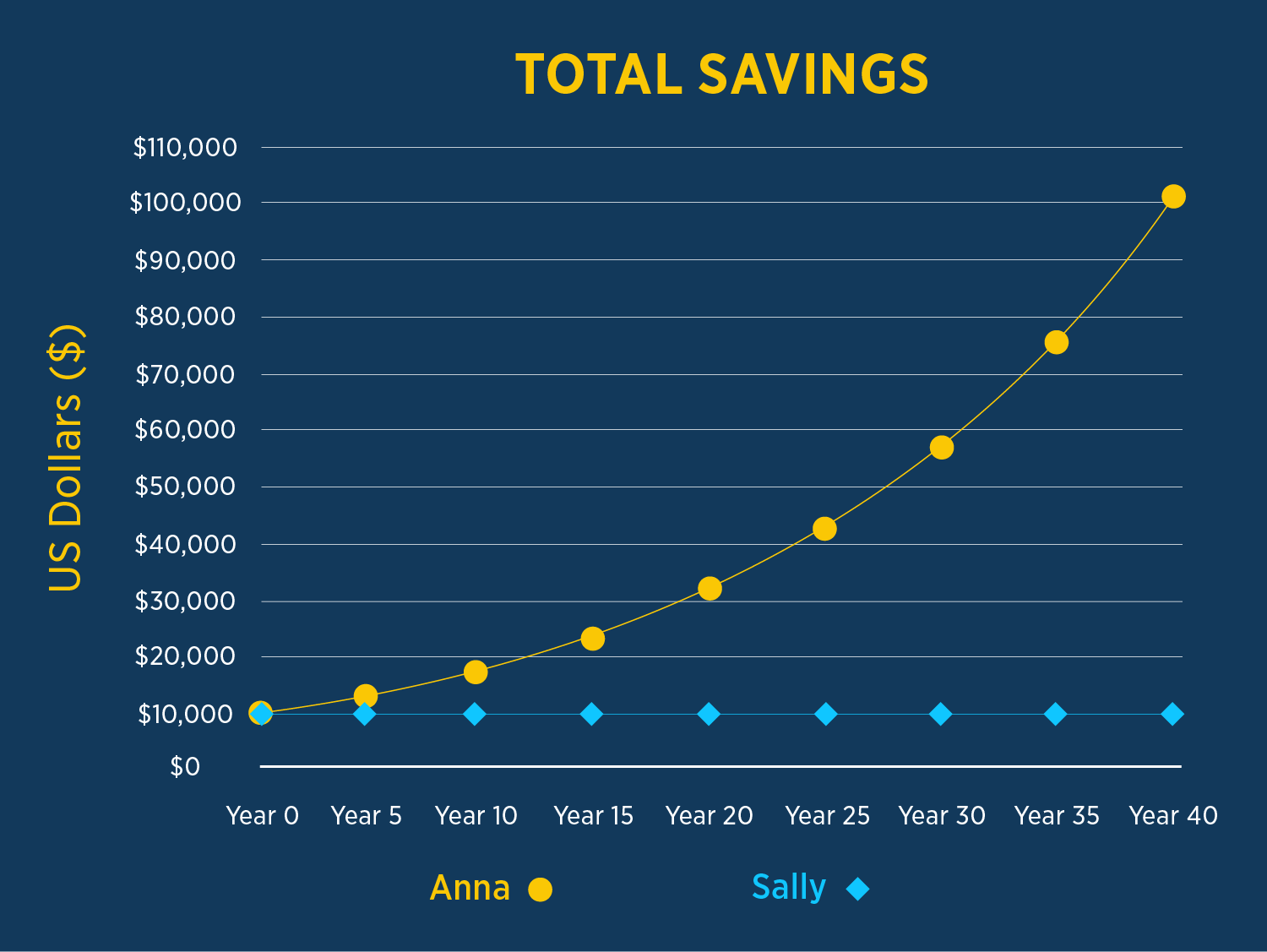

Let's look at an example to understand how compounding works. Sally and Anna both invest $10,000 into a hypothetical investment that earns 6% yearly. Sally decides to spend whatever she makes each year, while Anna allows her earnings to remain invested, giving it a chance to grow even more.

At the end of 40 years, how much do Anna and Sally have, respectively?

Since Sally spent all she gained, she only has $10,000. Anna, on the other hand, has $102,857. That includes her initial investment of $10,000, plus a whopping $92,857 in growth. When it comes to compounding, patience pays off. The graph below shows that Anna's growth really takes off in later years.