For investing newbies, the thought of putting money in the stock market can be scary. People often think getting into investing is too complicated or too difficult. As a result, they never get started, and they miss out on a valuable part of a long-term financial plan.

The truth is that investing is easier than most people think. It's kind of like when you purchase a new electronic device. It helps to read the instruction manual before you get started. When you know the basics, you feel more comfortable with it. Plus, you get a a whole lot more benefit out of it.

You could say the same for people who want to start investing. Understanding the basics can make the journey less stressful and more fun. Read on for our investing for beginners guide, filled with investing basics.

Part I: Stocks and bonds

What are stocks and bonds, and how do they work?

Stocks

In a nutshell, stocks are ownership shares of companies. These shares are bought and sold on exchanges, like the New York Stock Exchange, or NYSE, or the NASDAQ.

A share of stock is another way of referring to one unit of ownership in a business. Stocks are priced by the share and investors can buy full shares or, in some cases, fractional shares.

As with most investments, there's a risk that a stock's value, which is tied to the company's value and investor sentiment, will decrease or eventually become worthless. But the flip-side is also true. The value of the company and positive investor sentiment can both drive the stock price up.

Some stocks also pay dividends, which is a periodic payout that represents a share of the company's profits.

Bonds

Governments and companies can issue bonds when they want to raise money. Bonds are different from stocks because they are considered debt. So when investors buy bonds, they aren't actually buying ownership in the company, they're buying debt.

Think of it this way: If you buy a bond, you're loaning money to the company who issued it. In exchange, you get periodic interest payments based on the interest rate of that bond. When the bond matures, you get your initial money, also called principal, back. We often see bonds on local and state ballots for things like funding schools or building bridges. A vote for a bond gives your city or state permission to borrow money by selling bonds, often to banks, investment funds and individual investors.

While bonds are sometimes viewed as safer investments than stocks, there's still risk. Some bonds might even carry more risk than stocks, depending on the credit rating of the issuing company or agency. For that reason, it's wise to do your research.

When people don't have time to research market trends or analyze company financial sheets, they may not want to buy individual stocks and bonds. After all, tracking their values and making strategic decisions can be overwhelming. That's when they often turn to professional management through a brokerage.

Personally, I don't know how to replace the transmission on my car, so I take it to a professional who has been trained to do it. Sometimes, that's the best thing to do with investments, too.

Part II: Mutual funds and exchange-traded funds, or ETFs

In many cases, new investors turn to ETFs and mutual funds.

Mutual funds

Mutual funds are groups of investments also known as investment portfolios. They can include stocks, bonds and other assets. Whereas individuals might purchase a few shares of stocks, companies that manage mutual funds purchase lots of assets in quantities. They might, for example, hold $120 billion in assets spread out over hundreds or even thousands of companies.

Mutual funds can be both actively and passively managed. Actively managed mutual funds are under the management of qualified professionals who are paid to monitor the mutual funds. These managers make the buy-and-sell decisions to match their objective, which is often to achieve the highest return possible for their given risk appetite.

Passively managed mutual funds involve less buying and selling. So they usually track an index, like the Standard and Poor 500, better known as the S&P 500.

Different mutual funds also focus on different things. You can find mutual funds that focus solely on U.S. stocks and some that focus on international stocks. Some might focus on large companies, while others focus on small companies. If you're curious about a particular fund's investing philosophy, you can read its prospectus.

People are often drawn to mutual funds because they help provide diversification. Here's what that means: A mutual fund might invest in hundreds or thousands of stocks, so if you buy 10 shares of a mutual fund, you're not just buying 10 stocks. You're buying 10 units of thousands of stocks.

Investors buy and sell mutual funds once each day, after the U.S. stock market closes.

ETFs

ETFs are similar to passively managed mutual funds. But unlike mutual funds, ETFs can be bought and sold throughout the day, like a stock. For that reason, they look like mutual funds but act like stocks.

A passively managed mutual fund that tracks the S&P 500 may look very similar to an ETF that tracks the S&P 500, but they are different. They can be trading at different prices, have different expense ratios, and vary in performance. That's why it's always wise to do your research and ask questions before taking action.

Part III: Account types

While it's important to choose an investment that matches your personal financial situation and goals, it's equally important the account type fits as well.

Read on for an explanation of some of the most common account types.

Individual retirement accounts, or IRAs

IRAs can hold many different types of investment assets, including stocks, bonds, mutual funds and ETFs. They provide various tax benefits for saving, depending on whether the IRA is a traditional or Roth account.

Due to tax advantages, the IRS limits how much you can contribute yearly to IRAs.

401(k) or Thrift Savings Plan

For a lot of investors, 401(k)s, or employer retirement plans, are their first opportunity to begin saving for retirement. That's because when people get their first job, their employer asks how much of their paycheck they want to contribute.

Members of the military have access to the Thrift Savings Plan, or TSP, which is the military's 401(k).

This account is especially valuable if the employer offers matching 401(k) contributions. The military's Blended Retirement System offers such a matching contribution.

Like an IRA, the IRS limits how much investors can contribute to their employer retirement plan each year.

Regular taxable account

If investors have maximized contributions to account types that provide tax advantages, or if they need money before retirement, they might choose a taxable account.

With a regular account, investors receive no tax benefits and pay taxes yearly if taxes are due. But there are still some advantages.

If the investment is held for longer than one year before selling, any gains will be taxed at the long-term capital gains tax rate. This can be lower than the short-term capital gains tax rate that is taxed as ordinary income.

Part IV: First-timer common investing mistakes

When embarking on their investing journeys, many first-time investors often make the following three common investing mistakes:

Mistake 1: Not saving earlier

One of the most common questions is when to start investing.

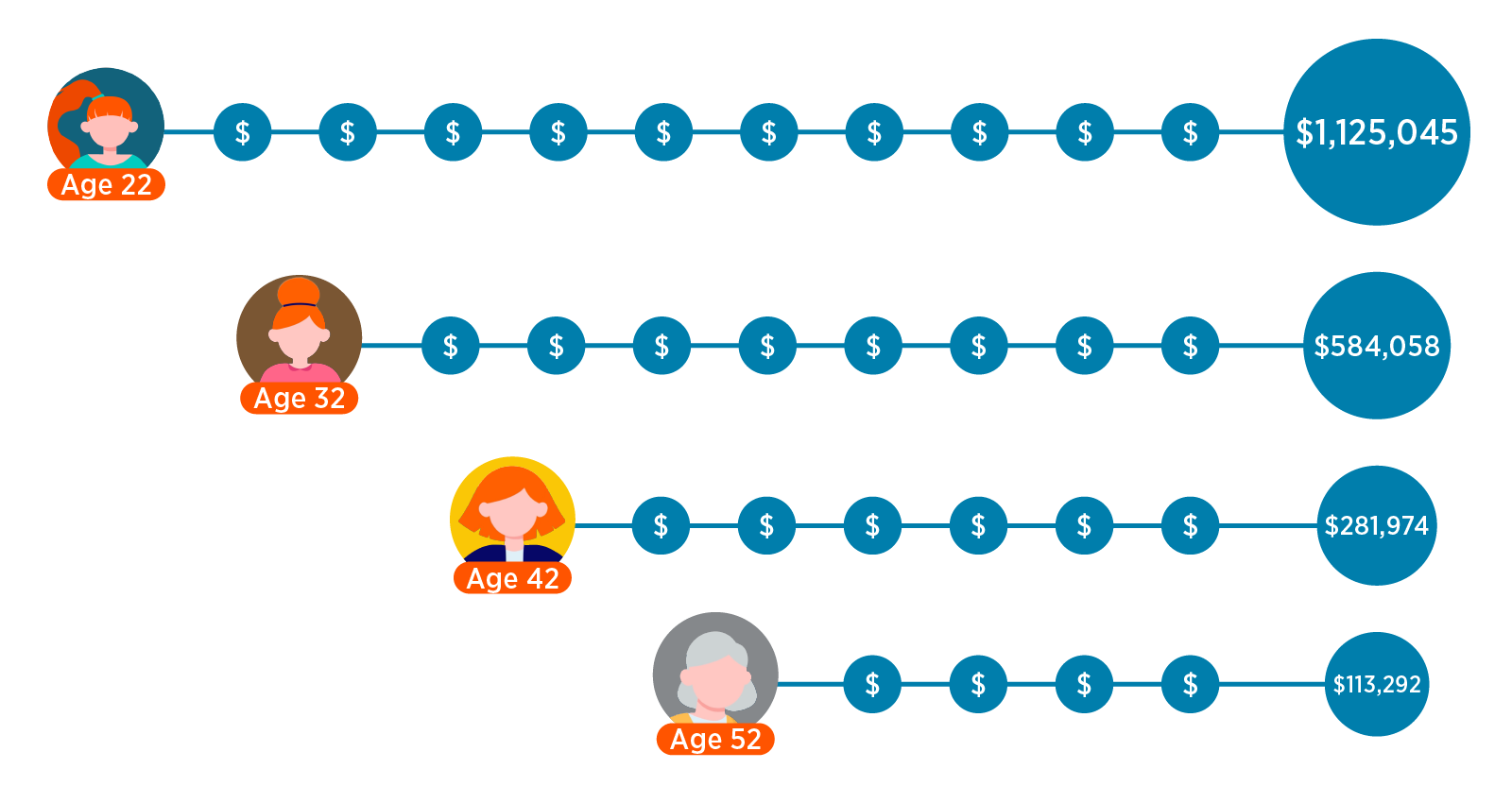

Let's say Sally invests $500 a month and earns a 6% return each year. Consider how much she stands to save by retirement, depending on how old she is when she starts investing:

- If she starts at age 22, she has over $1.1 million by retirement.

- Starting at age 32, she has over $580,000 by retirement.

- Starting at age 42, she has over $280,000 by retirement.

- Starting at age 52, she has just over $113,000.