Interest on a savings account: How your money can make money

When you learn how savings account interest works, you can get a better idea of when you'll reach your savings goals.

Free money probably sounds too good to be true, but it's possible if you understand how savings account interest works.

Interest is a charge for borrowing money. When you take out a loan or purchase items on credit, the bank will determine the interest rate to charge for the amount you borrow. That rate is based on the interest rate environment and other factors specific to the bank.

The roles are reversed when you open a savings account. The bank is essentially borrowing your money, and they will pay you interest to do so.

While interest on a savings account isn't necessarily the fastest way to build wealth, the amount deposited isn't subject to market risk, so it'll steadily add a bit more money to your balance than what you had when you opened the account — and you don't have to do anything but collect.

What's the difference between simple and compound interest?

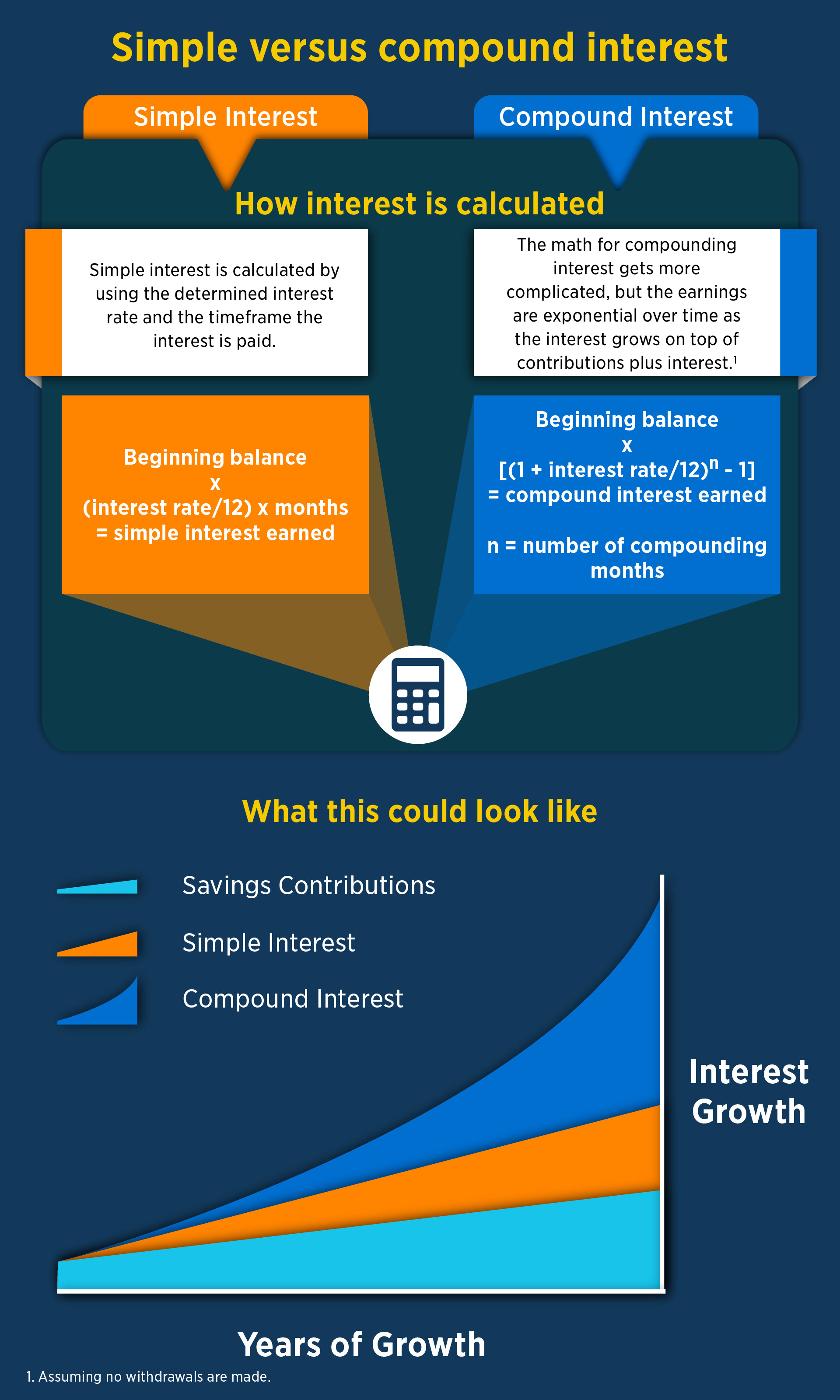

- Simple interest is how much you earn monthly on the amount originally deposited into your savings account.

- Compound interest is how much you earn on the original deposit amount and the monthly interest accrued in the account. In other words, it's interest on interest.

How to calculate interest on a savings account

Simple interest is calculated by using the determined interest rate and the timeframe within which the interest is paid. Let's assume interest is paid monthly:

You earn more interest when you have larger account balances and leave the money in the account for longer periods of time.

What's the difference between the APY and interest rate?

- APY stands for annual percentage yield. It's the amount of interest on a savings account you would earn over a year, and it includes compounding interest.

- Interest rate is the amount of stated interest being paid by the bank without taking into account the compounding effect.

Interest rates can help you decide how to save.

Different banks offer different APY rates, advertised as percentages, for different types of accounts.

Some banks even offer a higher interest for larger dollar amounts deposited.

Compare the APY of multiple banks when you're shopping for the bank for you. Also, look at the various savings solutions the bank offers. The higher the APY percentage, the more interest you'll earn and the faster your money will grow.

It's important to note that some interest rates can fluctuate in response to the activities of the Federal Reserve. That's why on your bank statements you might see varying amounts of earned interest on a savings account. If the federal rate increases, banks will typically follow suit. If the federal rate decreases, so too will the banks'.

How banks pay interest on a savings account

The bank deposits savings account interest payments directly into the account. Interest is one way to more quickly achieve your goals like saving for a new home or an emergency fund.

APYs aren't the only consideration though, as you'll also want to consider things like fees, withdrawal limitations, digital capabilities and money transfer options. Fees in particular are important because they could negate the interest you earned, so be sure to consider all factors. But in the end, compound interest earned in a savings account can be a great way to accomplish short-term financial goals.

The USAA Advice Center provides general advice, tools and resources to guide your journey. Content may mention products, features or services that USAA Federal Savings Bank does not offer. The information contained is provided for informational purposes only and is not intended to represent any endorsement, expressed or implied, by USAA or any affiliates. All information provided is subject to change without notice.