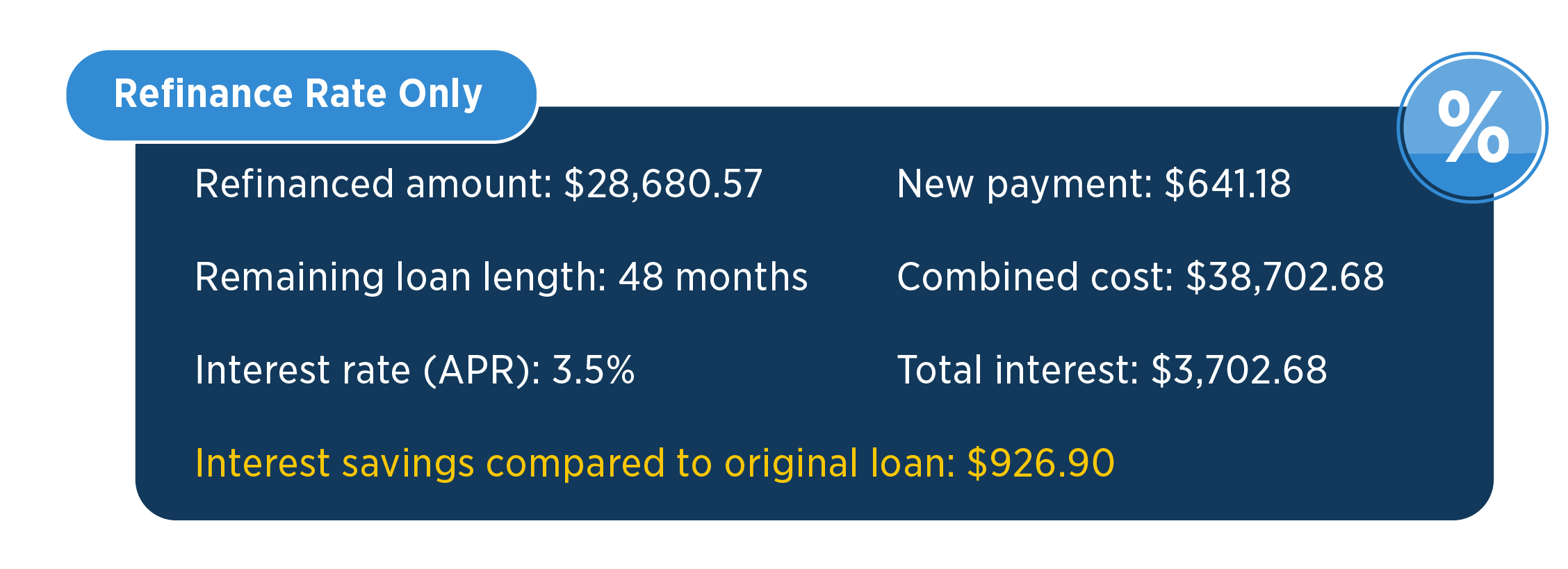

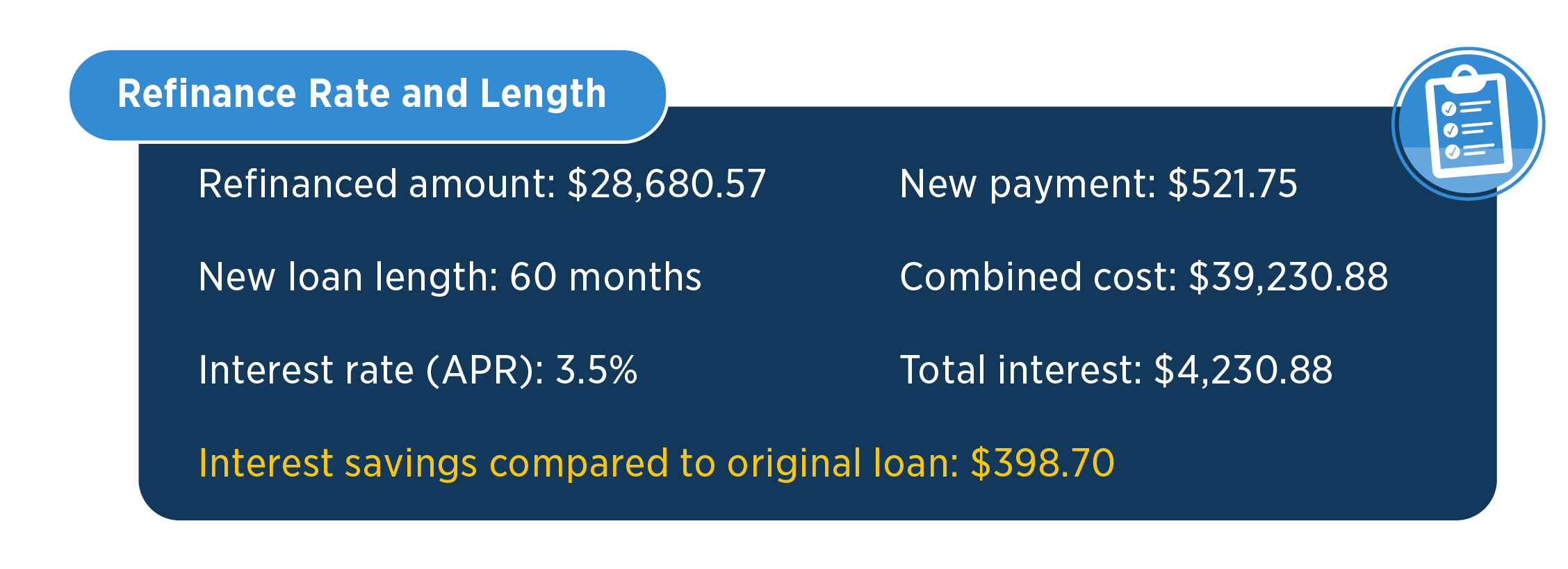

Assume that you refinance your remaining balance for 60 months at a new interest rate of 3.5%, your new payment is $521.75. In this scenario, you’ll have saved about $140 a month and almost $400 in total interest.

Key takeaway: If rates are lower today than when you first took out your loan, it may present an opportunity to save over the life of your loan.

What about my car’s value?

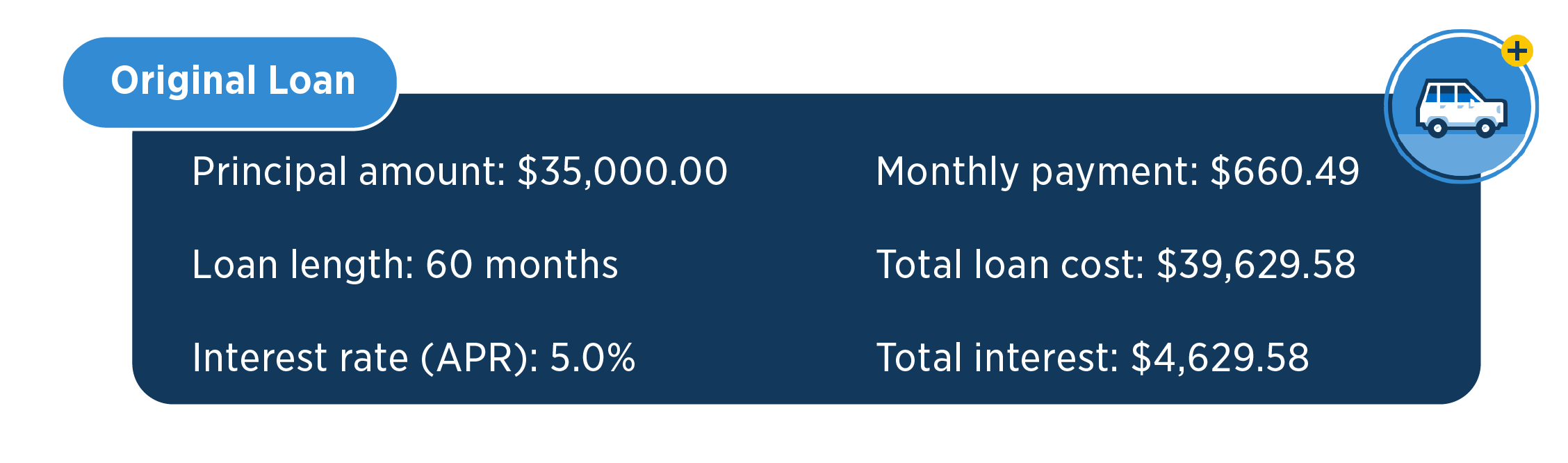

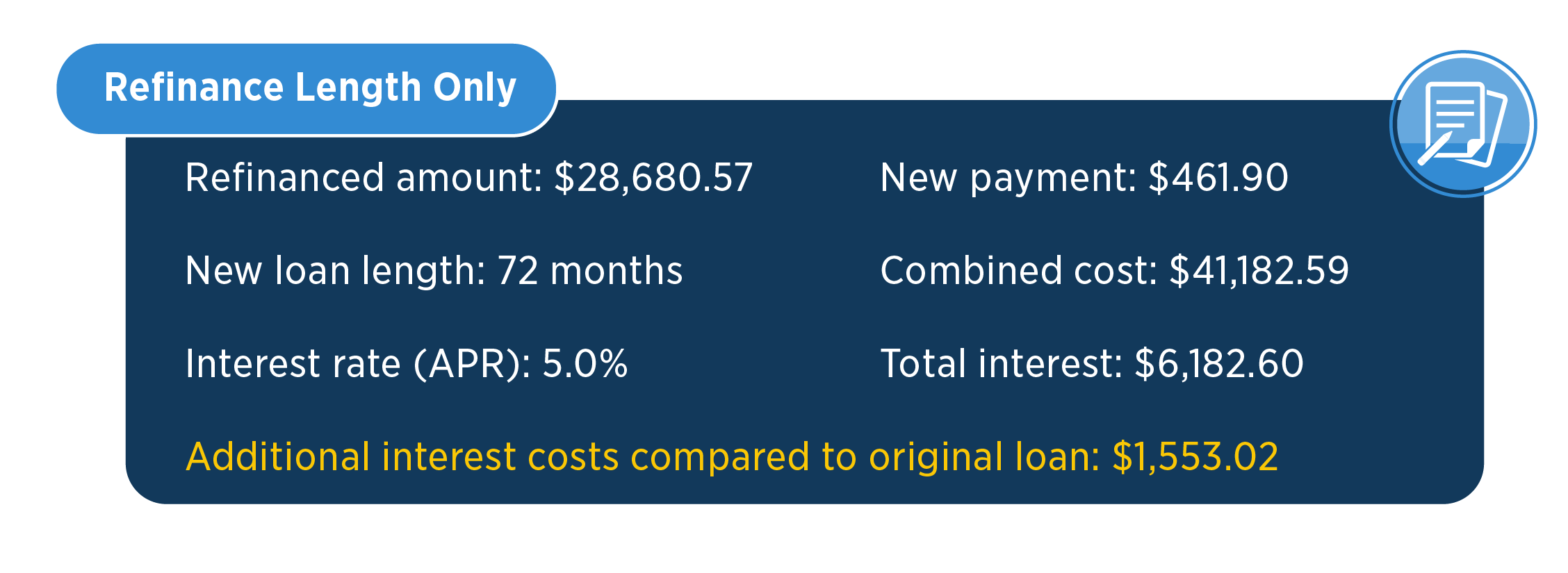

You may be looking for ways to save and are considering refinancing for a lower payment but at a longer loan term. This could be a short-term gain on your monthly payment but a long-term cost in interest and potential loss of equity.

Ideally, you can sell your car for more than what you owe on it and can put that money towards a new car purchase in the future.

Cars typically depreciate. New cars lose the most value within the first year on the road. After five years, your new car may be worth 40% less than you purchased it for. You could see your loan balance exceed the value of your car. This is commonly called being “upside-down.”

Being upside-down in your current car can impact your future car purchases. It could also leave you in a tight spot financially if your car is stolen or totaled in an accident. Your bank or lienholder gets paid first in an insurance claim for a total loss. Unless you have things like GAP insurance or a car replacement benefit on your auto policy, you could be on the hook for the difference between your loan balance and insurance settlement amount.

What else do I need to know?

It’s important to know all the details you can about your current loan and any loan offers you’re considering. While rare, your current loan may have a prepayment penalty for paying the loan off sooner than scheduled. Your new loan may have loan origination costs or other fees that are built in. Read through your loan documents and make sure to include any fees that you may have in your calculations.

According to research by Bankrate®, the average prepayment penalty is about 2% of the remaining loan balance. Revisiting the scenarios from this article, that could mean paying an additional $573 to refinance your car. Prepayment fees are only allowable in some states and are prohibited on longer term loans, so check your loan documents to see what you may or may not have.

Similarly, origination fees can range 1-2% of the total amount borrowed. In our scenario, that would add about $280-573 bucks if your new loan provider charges an origination fee.

There may also be optional programs, like warranties or insurance policies, wrapped into your loan that could be impacted if you refinance. Look out for things like credit life insurance and GAP protection. These programs typically provide benefits that are tied to the loan balance. If you want those programs on your new loan, speak to your new loan provider to see if they’re offered.

Is refinancing right for me?

Crunch the numbers. If you can save money on both the total interest paid and your monthly payment, it may be a good idea to refinance. Saving money on your payment alone may not be ideal, whereas saving money on the total interest is preferred.

Do some research on rates, terms and get help from tools like USAA’s auto loan calculator. See note 1 Having numbers for refinancing can help you weigh out the options and help you make the best decision for your unique situation.